Economist and gold bug Peter Schiff has warned that high inflation will return with a vengeance and significant Fed rate hikes will be necessary. He also criticized JPMorgan CEO Jamie Dimon for downplaying the severity of the U.S. economic situation. However, he conceded that Dimon’s perspective is “a lot closer to being right than most […]

Economist and gold bug Peter Schiff has warned that high inflation will return with a vengeance and significant Fed rate hikes will be necessary. He also criticized JPMorgan CEO Jamie Dimon for downplaying the severity of the U.S. economic situation. However, he conceded that Dimon’s perspective is “a lot closer to being right than most […]

Bitcoin News

UN Accuses North Korea Of $3B Crypto Theft To Fund Nuclear Weapons Program

In a recently reviewed unpublished report by Reuters, United Nations (UN) sanctions monitors have alleged that North Korea engaged in a massive theft of crypto assets, raking in billion through cyberattacks.

Nuclear Upgrades And Crypto Cyberattacks Unveiled

According to Reuters, the independent panel of sanctions monitors revealed that despite international sanctions, North Korea continued to defy regulations by enhancing its nuclear arsenal and producing nuclear fissile materials.

The monitors further noted that the country conducted ballistic missile launches, deployed a “tactical nuclear attack submarine,” and even placed a satellite into orbit.

The UN report points to 58 suspected cyberattacks on crypto-related companies between 2017 and 2023, valued at approximately billion. These attacks allegedly provided crucial funding for North Korea’s weapons of mass destruction (WMD) development.

The report states that hacking groups affiliated with the Reconnaissance General Bureau, North Korea’s primary foreign intelligence agency, were responsible for these cyber assaults.

The monitors highlighted the increasing trend of North Korea targeting defense companies and supply chains and collaborating with other actors by sharing infrastructure and tools. The report also raises concerns about reports of North Korea supplying conventional arms and munitions, which contravenes existing sanctions.

While the UN report is set to be released publicly later this month or early next, North Korea’s mission to the United Nations has not yet responded to requests for comment on the sanctions monitors’ allegations.

The Security Council, traditionally deadlocked on the issue, is unlikely to take immediate action against North Korea, according to Reuters.

China and Russia have advocated for easing the sanctions to “persuade” North Korea to return to denuclearization talks. Furthermore, Russia and North Korea have recently pledged to strengthen military relations, although both countries deny allegations of weapons supply.

North Korea’s Illicit Trade

Per the report, North Korea has slowly begun to emerge despite the lockdown imposed amid the COVID-19 pandemic. The UN report reveals signs of trade recovery, with a higher trade volume in 2023 compared to 2022.

Notably, the United Nations monitors noted the reappearance of foreign consumer goods, including potential luxury items prohibited under Security Council sanctions.

The sanctions monitors also investigated reports of numerous North Korean nationals working overseas violating sanctions, particularly in information technology, restaurants, and construction sectors. These individuals were found to earn income that benefited the North Korean government.

In addition, the report highlights North Korea’s continued access to the international financial system and engagement in illicit financial activities, including crypto assets, in defiance of UN Security Council resolutions.

Featured image from Shutterstock, chart from TradingView.com

Minnesota Power Co-op Accuses Couple of Major Electricity Theft for Bitcoin Farm Operation

In a case that intertwines crypto mining and utility theft, a Minnesota power company, North Star Electric Cooperative, has accused a former couple, Ryan Jaenicke and Tina Fehlhaber, of stealing vast amounts of electricity. The alleged scheme, detailed in a 19-page civil suit filed in Roseau County Court, was purportedly to power a bitcoin farm in Roosevelt. This revelation follows North Star’s discovery last year of a significant loss of power in its distribution network.

Alleged Utility Theft for Bitcoin Mining Leads to Lawsuit Against Minnesota Couple

According to a report, North Star, a not-for-profit, member-owned power distribution cooperative, first noticed a substantial loss of electric power in June 2022, sparking an investigation. During a routine inspection in May 2023, employees uncovered non-North Star equipment connected to their lines in Roosevelt, leading to a property owned by Fehlhaber. Inside, they found two unauthorized 50 kilovolt-ampere transformers and over two dozen cryptocurrency mining units.

Jaenicke, known for his Youtube channel “Degenerate Passive Income,” is accused of being the mastermind behind this operation. In his videos, he often discussed cryptocurrency as a lucrative passive income source, even showing off his mining farms. However, it’s alleged that the Roosevelt farm operated on stolen electricity from North Star, resulting in losses potentially amounting to hundreds of thousands of dollars.

The lawsuit uploaded by theminermag.com and brought forth by North Star details the extensive nature of the alleged theft. It’s unclear if others were involved in what appears to be a well-orchestrated scheme. Additionally, attempts by Jaenicke to allegedly bribe a North Star employee for more power access were rejected. While the Roseau County Attorney’s Office initially declined to prosecute due to insufficient evidence, this decision could change if new evidence emerges.

North Star’s lawyer, Joel Fremstad, emphasized the severity of the theft, comparing the electricity consumption to that of a school or a commercial building. The cooperative has disconnected the unauthorized equipment and reported the case to law enforcement. They are seeking at least ,000 in damage compensation and the disgorgement of all profits obtained through the alleged electricity theft.

“At the heart of it we see theft and greed,” the lawyer for North Star told the news publication inforum.com.

Jaenicke, owner of Northland Tire in Roseau, and Fehlhaber, have not been reachable for comments. Local reports note that the couple, who recently separated, could face significant financial repercussions if found liable. Under Minnesota law, they could be forced to pay double the amount of electricity stolen plus any profits from the crypto mining.

What do you think about the couple accused of stealing electricity to mine bitcoin? Share your thoughts and opinions about this subject in the comments section below.

Inside Caroline Ellison’s Explosive Testimony — Former Alameda CEO Accuses SBF of Directing Fraud at FTX

In bombshell testimony on Tuesday, Caroline Ellison, former CEO of Alameda Research, accused Sam Bankman-Fried of directing her and others to commit fraud under his leadership at FTX and Alameda. Taking the stand in a red dress, Ellison stated “Alameda took several billions of dollars from FTX customers and used it for investments.”

Caroline Ellison Exposes Alleged FTX Fund Siphoning and Political Payoffs

According to reporting by Matthew Russell Lee of Inner City Press, who streamed the proceedings from the courtroom, Caroline Ellison detailed how she and her colleagues improperly used billions in customer funds from FTX to pay back loans and make speculative investments for Alameda Research.

Lee reported that Ellison claimed she engaged in fraud at Sam Bankman-Fried‘s direction, alleging he “set up the systems and told us to take the money.” The former Alameda CEO estimated that between to billion in FTX customer funds were deposited into Alameda accounts and used for the crypto hedge fund’s purposes. Federal prosecutor Danielle Sassoon asked Ellison directly how Alameda also defrauded its lenders.

Ellison stated:

I sent balance sheets that made Alameda look less risky than it was.

When asked by prosecutors if she was concerned about Alameda tapping FTX customer funds, Ellison admitted she thought customers were unaware and that Bankman-Fried told her “not to worry” and that auditors wouldn’t look into it. She also described helping prop up the price of FTX’s native token FTT by purchasing it when the price fell below , allegedly at Bankman-Fried’s urging. She explained the ins and outs of Alameda’s mystery bank account dubbed “fiat@.”

Ellison’s testimony directly implicated Bankman-Fried in the alleged fraud scheme. Her statements appear to support federal prosecutors’ charges that the founder of FTX misappropriated billions in customer funds to cover losses at Alameda Research. Ellison’s account also highlighted the blurred lines between the two companies under Bankman-Fried’s leadership. Ellison also mentioned all the political donations FTX executives gave U.S. bureaucrats. She stated:

Sam gave million to Biden, he thought it bought him access.

Ellison touched on her intermittent romantic ties with the ex-FTX chief over the years. The spotlight remains on Ellison’s testimony, set to resume tomorrow, while prosecutors anticipate summoning more witnesses as the week progresses. Her account stands as the most incriminating testimony against Bankman-Fried to date.

What do you think about Ellison’s testimony against Bankman-Fried? Share your thoughts and opinions about this subject in the comments section below.

Deflecting Blame — Bank of England Governor Bailey Accuses UK Retailers of Overcharging Customers

After the Covid-19 pandemic, many people believe the implementation of extensive stimulus measures and quantitative easing (QE) policies resulted in an overwhelming surge of inflation that has burdened millions across the globe. While certain individuals attribute this economic turmoil to the actions of central banks, Andrew Bailey, the governor of the Bank of England, firmly asserts that it is the retailers who are guilty of overpricing goods and services, consequently causing distress among countless families in the United Kingdom.

Bank of England Boss Andrew Bailey Pulls out the ‘Greedflation’ Accusation From the Bureaucratic Tool Box

Although central banks have often been accused of bearing the brunt of responsibility for the economy’s volatile boom and bust cycles, their leaders refuse to shoulder the blame alone. European Central Bank (ECB) president Christine Lagarde, for instance, attributes Europe’s relentless inflation to the impact of climate change. Meanwhile, in an interview with the BBC, Andrew Bailey, the governor of the Bank of England, contends that it is the retailers who are placing an undue burden on U.K. citizens.

In his interview, Bailey strongly emphasized that the burden of “overcharging customers” falls squarely on the shoulders of retailers, ultimately contributing to the unwelcome surge in inflationary pressures. “If you look at petrol prices, some sellers of petrol have possibly been charging too much for it,” Bailey insisted. When questioned about the potential timeline for a reduction in the benchmark bank rate, the governor of the Bank of England found it challenging to provide a definitive answer. Bailey stated:

I can’t give you a date as to when interest rates start to come down because that really depends upon what happens over the period of time ahead, but getting inflation down is the most important thing that we have to do.

Despite Bailey’s assertions, U.K. retailers are dismissive of the argument he presents, and Martin Scicluna, the chair of Sainsbury’s, the country’s second-largest grocery store, vehemently refuted the accusation, deeming it false. “To be very, very clear, we are not profiteering and we are not rip-off retailers,” Scicluna firmly stated.

This sentiment is shared by Alex Baldock, the CEO of Currys, an electrical retailer, who emphasized that the company has effectively managed to keep “a lid on price rises.” Moreover, the notion of “greedflation,” often propagated by bureaucrats and central bankers in an attempt to deflect blame from their own failed economic policies, garners limited support among people worldwide.

Within the United States, Democratic leaders are convinced that the surge in inflation can be attributed to nothing but unbridled corporate greed. Last year, Elizabeth Warren, the Democratic senator from Massachusetts, put forth the “Price Gouging Prevention Act of 2022” in response to this concern. However, this argument has faced extensive criticism.

Blogger Matthew Yglesias astutely pointed out the fallacy of “greedflation” last year, meticulously highlighting the plethora of inconsistencies and logical gaps within this theory when compared to actual facts, data, and rational thinking. Yglesias aptly remarked, “At the end of the day, though, only a very stupid person would think companies suddenly became greedy in 2021 after years of being non-greedy.”

What are your thoughts on Governor Bailey’s claim that retailers are to blame for rising inflation? Do you agree or disagree? Share your thoughts and opinions about this subject in the comments section below.

Economist Steve Hanke Warns of an ‘Ugly’ Recession Looming and Accuses Federal Reserve of Directionless Policies

Steve Hanke, an economist and professor of Applied Economics at Johns Hopkins University, as well as a former member of Ronald Reagan’s Council of Economic Advisors, recently expressed his belief that the U.S. Federal Reserve is lacking direction and “doesn’t know what it is doing.” Hanke further predicts a bleak economic downturn in 2024, referring to it as an “ugly recession.”

Steve Hanke: ‘I Think the Fed Doesn’t Know What It’s Doing’

During a recent interview with Kitco News’ lead anchor Michelle Makori, economist Steve Hanke delved into the future of the U.S. economy and the Federal Reserve’s recent decision to halt the federal funds rate at the Federal Open Market Committee (FOMC) meeting held on Wednesday.

Hanke emphasized that while the interest rate garners significant attention, it is the monetary supply that warrants closer scrutiny. He pointed out that Federal Reserve chairman Jerome Powell acknowledged the continuation of quantitative tightening despite the pause in rate hikes.

Hanke said the money supply has been contracting since last April, and he noted that it has shrunk by 4.6%. He emphasized that one would have to go back to 1938 or 1939 to “find that kind of shrinkage.” The economist insisted that contractions and expansions in the money supply will transmit changes throughout the economy, and within about six months, there will be changes in sensitive asset prices.

He commented that if you look ahead 12 to 24 months, “you get changes in broad-based inflation so what we’ve seen here is that since the money supply peaked.” “What does that mean?” Hanke asked himself. “That means the economy is going to be crashing.” The economist emphasized that “inflation is falling very rapidly because the money supply has been contracting very rapidly.” Hanke added:

Eventually, we’re going to have the economy contracting very rapidly.

The economist said that the Fed doesn’t pay much attention to the money supply because it believes the money supply is “not a reliable indicator.” Yet Hanke insists they are “ignoring the evidence” and the “models that they have are post-Keynesian macroeconomic models that don’t include money.” Hanke wholeheartedly believes a “recession is baked in the cake given these money supply contractions.” Due to economic lag, Hanke said it could be anywhere between six to eighteen months.

“I think the Fed doesn’t know what it’s doing,” he told Makori. “Remember they have doubled down on this money supply business and chairman Powell has repeatedly said in public the Fed doesn’t pay any attention to the money supply.”

Hanke said that banks are now tightening and reducing assets to “meet the demands of the regulators.” He believes that the Fed could change its approach if there’s a “credit crunch on Wall Street.” “The only thing that could make them pivot is if they have some kind of credit or liquidity crash, or squeeze on Wall Street,” Hanke said.

The economist has long been critical of the Federal Reserve, and during the conversation with Makori, Hanke also discussed gold. He expressed a positive outlook on gold, citing its past performance during recessions. He also mentioned how central banks were purchasing lots of gold in recent times. Hanke concluded by discussing how inflation should be handled in Argentina.

What are your thoughts on Steve Hanke’s warning about an ‘ugly’ recession and his critique of the Federal Reserve’s direction? Share your insights and opinions in the comments section below.

Bitcoin Advocate Nic Carter Accuses ‘Laser-Eyed Maxis’ of Turning Bitcoin Into a ‘Secular Cult’

In a tweet this week, crypto advocate Nic Carter took aim at those who claim to be bitcoin enthusiasts but have been applauding the U.S. Securities and Exchange Commission’s (SEC) enforcement actions. Carter accused these individuals of turning Bitcoin into a “secular cult” and argued that the “vast majority” of them are actually newcomers to the cryptocurrency space. His criticism highlights the growing divide within the Bitcoin community between those who prioritize decentralization and those who welcome regulatory oversight.

Nic Carter ‘Laser Eyes or Bitcoin Maximalism Isn’t Like a Religion, It’s Literally One — It Has Everything a Religion Has’

As of late, a number of Bitcoin advocates have been seemingly cheering on the U.S. Securities and Exchange Commission’s (SEC) enforcement actions against major exchanges like Binance and Coinbase. These individuals argue that all cryptocurrencies except for bitcoin (BTC) are unregistered securities and have been eagerly awaiting the SEC’s crackdown. However, longtime Bitcoin supporter Nic Carter took to Twitter to criticize this group, claiming that they have turned Bitcoin into a “secular cult.” In a lengthy tweet, Carter accused these so-called “bitcoiners” of blindly following a dogmatic belief system.

#Bitcoin maxis have saved MILLIONS.

Crypto has lost BILLIONS.

We are not the same. pic.twitter.com/r4KliZkYvY

— The ₿itcoin Therapist (@TheBTCTherapist) June 7, 2023

“[You can call this group] ‘laser eyes’ or ‘maxis,’ whatever you want, they know who they are, we know who they are,” Carter said. “There’s no uncertainty about this – they are people that elevated Bitcoin from a mere tool to a belief system, a way of life. The vast majority of these cult adherents are actually new to Bitcoin,” he added. According to Carter, this group of Bitcoin enthusiasts peddles false promises of wealth and endless price growth. He also noted how they have bought into “fallacies like the stock-to-flow model.”

Carter stressed:

Again, remember that these are latecomers. They needed to find a moral high ground over the established crypto elites, that mostly made money from their participation in the space, and the pure, underprivileged Bitcoin plebs.

Carter’s criticism of this group of Bitcoin enthusiasts didn’t sit well with everyone. One person accused him of being too focused on short-term gains, arguing that simply “stacking” Bitcoin would have yielded better returns all along. Another individual questioned Carter’s assertion that the majority of these enthusiasts are newcomers to the space. “I’m curious where you draw the conclusion that Bitcoin maximalists are new to the space,” the person asked. Carter’s response was blunt: “Because I have eyes.” While some agreed with Carter’s sentiment and expressed their own frustration with Bitcoin maximalists, others dismissed his comments as nothing more than a rant.

One of the most absurd threads I ever read. If Coinbase just focused on Bitcoin, it would be irrelevant as a company. The reason why Coinbase matters is that they embraced the innovation that happens across the industry.

And bitcoin maxis cheering excessive & arbitrary… https://t.co/67kIKEwjzB

— Brian Fabian Crain (@crainbf) June 7, 2023

Carter’s viewpoint was met with opposition from an individual who claimed to have been a “hardcore maxi” since 2016. This person shared their experience of stacking sats and withdrawing their bitcoin from exchanges. In a lengthy response, they vehemently disagreed with the notion of using centralized exchanges and entrusting them with one’s bitcoins. According to them, this practice is even worse than relying on banks to hold one’s money. He added:

Coinbase and Binance need to fail they hold way to much customer bitcoin. It needs to be withdrawn immediately from all these exchanges. My profile was created in 2011. I’m honestly surprised you haven’t blocked me yet because of laser eyes.

In his tweet, Carter didn’t hold back in his criticism of BTC maximalists, claiming that they aren’t interested in building real companies. Instead, he argued, they’re more like members of a religious cult, complete with their own set of religious texts, a conception myth, eschatology, rituals, and even a tithe. According to Carter, these cultists take issue with exchanges like Binance and Coinbase because they listed other cryptocurrencies, which they see as “impure.” This is despite the fact that these exchanges have “done more for bitcoin adoption and accessibility than literally any other companies in the industry’s history,” he said.

While Carter acknowledges that Binance and Coinbase may have made some questionable decisions, he also recognizes that they are two very different companies with different regulatory strategies. Despite this, he believes that “they did provide the tools for bitcoin to achieve global adoption in a way that wasn’t possible before.” Carter’s criticism of Bitcoin tribalism is nothing new, as the community has been grappling with issues and debates associated with altcoins and block size scaling for years.

More recently, there has been a growing chorus of voices arguing that non-fungible tokens (NFTs) and BRC20 tokens have no place on the Bitcoin network. This has sparked a fierce debate within the community, with some ‘laser-eyed maxis’ arguing that the Bitcoin blockchain should be used exclusively for financial transactions.

What do you think about Nic Carter’s opinion of laser-eyed maximalists? Share your thoughts and opinions about this subject in the comments section below.

Nigeria-China Currency Swap: Activist Lawyer Accuses IMF and World Bank of ‘Economic Sabotage’ to Promote US Dollar, Urges Nigeria to Join BRICS

Nigerian human rights activist and lawyer, Femi Falana, has accused the International Monetary Fund (IMF) and the World Bank (WB) of sabotaging the currency swap arrangement between China and Nigeria. Falana said the Nigerian central bank and the two global financial institutions are helping to perpetuate “the dominance of the United States dollar in Nigeria.”

Nigerian Federal Government Accused of Dollarizing the Economy

The International Monetary Fund and the World Bank are conniving with the Central Bank of Nigeria (CBN) to sabotage the country’s currency swap arrangements, Nigerian human rights activist Femi Falana has said. In his statement published by The Punch, Falana, who is pushing for Nigeria to join Brazil, Russia, India, China, and South Africa in the BRICS bloc, has also accused the Nigerian federal government of continuing to dollarize the economy while other nations are trying to promote their own currencies.

The claims by Falana, a lawyer, follow revelations that his country’s currency swap arrangement with China has not benefited Nigeria. As reported by Bitcoin.com News in April, some Nigerian economic experts believe the country’s five-year-old currency swap agreement with China has failed to ease pressure on the local currency. The experts believe a trade imbalance between the two countries to be one of the reasons the swap arrangement failed.

‘Economic Sabotage’

In his statement, Falana appeared to acknowledge that the swap arrangement had not achieved what Nigerian officials had hoped for. However, the activist lawyer said the collusion between the two international financiers and the CBN had made it impossible for the currency swap arrangement to work. He explained:

The International Monetary Fund and the World Bank which superintend the Central Bank of Nigeria have colluded with the Central Bank of Nigeria to frustrate the currency swap. The purpose of the economic sabotage is to promote the dominance of the United States Dollar in Nigeria. Even though Nigeria has since become an important source of oil and petroleum for China’s rapidly growing economy, the Federal Government has continued to demand payment in dollars instead of nairas.

Falana also railed against the Nigerian government’s failure to follow in the footsteps of other countries that have signaled their intention to join BRICS.

The lawyer also chastised the CBN’s controversial currency redesign policy which led to the widespread shortage of naira banknotes. He argued that instead of pursuing the so-called naira redesign policy, the Nigerian government should move to renew the currency swap arrangement with China. Falana added that similar swap arrangements “with other friendly nations” should also be made.

Register your email here to get a weekly update on African news sent to your inbox:

What are your thoughts on this story? Let us know what you think in the comment section below.

South African Professor Accuses US Regulators of Attempting to ‘Assassinate Crypto’

The United States’ attempts to “assassinate crypto” are illegal and unlikely to succeed because “crypto is global,” Steven Boykey Sidley, a South African professor and author, has argued. According to Sidley, many formerly U.S.-based companies and innovators have fled the country and have set up bases in countries with more “comfortable” regulatory environments.

The United States’ Agenda Against Crypto

Steven Boykey Sidley, a South African professor of practice at JBS, University of Johannesburg, has accused U.S. regulators and departments of orchestrating what he described as coordinated and “possibly illegal” efforts to “assassinate crypto.” Sidley insisted that there are no moral or legal grounds justifying the attempts to take out BTC, particularly when the world is in the midst of a banking crisis sparked by banking failures in the U.S.

In his op-ed published by the Daily Maverick, Sidley points to the U.S. Federal Reserve’s “opaque and non-explanatory” reasons for refusing to grant a national banking license to Custodia Bank as one example of how U.S. authorities are attempting to kill crypto. According to the professor, the bank and its founder Caitlin Long were committed to reducing risks and boosting depositors’ confidence “that their deposits into crypto-exchanges were backed 1:1.”

Sidley asserts in the op-ed that the U.S. Federal Reserve’s abrupt and inexplicable withdrawal from its engagements with Custodia suggests that the United States has a sinister agenda against cryptos.

Coordinated Attacks

Meanwhile, Sidley also highlighted how U.S. regulators have seemingly coordinated their actions against crypto entities.

“Curiously coincidental in time, sometimes happening within hours of a seemingly unrelated announcement from some different corner of government. Keep in mind, some of the bodies are supposed to be entirely independent – they are designed not to collaborate for excellent reasons of conflict avoidance,” Sidley said in the op-ed.

Despite what he sees as illegal acts by U.S. regulators, Sidley, the co-author of the book Beyond Bitcoin: Decentralised Finance and the End of Banks, insisted powerful opponents like U.S. senator Elizabeth Warren are still unlikely to get their way, because “crypto is global.” He claimed that many formerly United States-based companies, developers, and innovators have already moved to places like Dubai, Hong Kong, Singapore, and Switzerland where the regulatory environment is more “comfortable.”

What are your thoughts on this story? Let us know what you think in the comments section below.

Coinbase Exec Accuses Binance Of Crypto Price Manipulation

The world’s largest cryptocurrency exchange Binance was in the crossfire of critics for a long time after the FTX collapse. In particular, there was harsh criticism because of an opaque proof of reserves issued by the auditing firm Mazars, which paused the cooperation with the exchange shortly thereafter.

Over the turn of the year, however, the criticism has become quieter and Binance has disappeared from the spotlight as DCG and Genesis became the crypto industry’s biggest headache. But Conor Grogan, Head of Product Business Operations at Coinbase, presented new serious allegations against Binance today.

In a Twitter thread, Grogan wrote that there is a “pattern of Binance front-running over 18+ months.” He found Binance-connected wallets which were buying 0.000 RARI seconds before the listing and dumped them minutes after.

He also found an incident where around 78,000 ERNs were bought between June 17th and 21st and sold immediately after the listing was announced. The same thing was done with TORN, where “hundreds of thousands were bought and sold right after the announcement.”

Another example is the purchase of RAMP, worth more than 0,000, of over multiple days, “before sending it to Binance minutes after the listing announcement. Assuming they sold it was a ~100K payday.” Grogan explained:

I found all of these via looking at the original wallet’s OKX deposit address and looking at the other counterparty wallets. Not great opsec by them. I just started digging in so there might be more examples.

According to the Coinbase exec, the front-running could have a variety of causes. Most likely, according to Grogan, is insider MNPI (Material Nonpublic Information) which is operated by a rogue employee who is connected to the listing team and has details of new asset announcements.

Another explanation could be a trader finding a leak in an API or test trade exchange. In any case, regulators and law enforcement agencies are likely to be very interested in the case, as evidenced by the recent cases against Coinbase for insider trading.

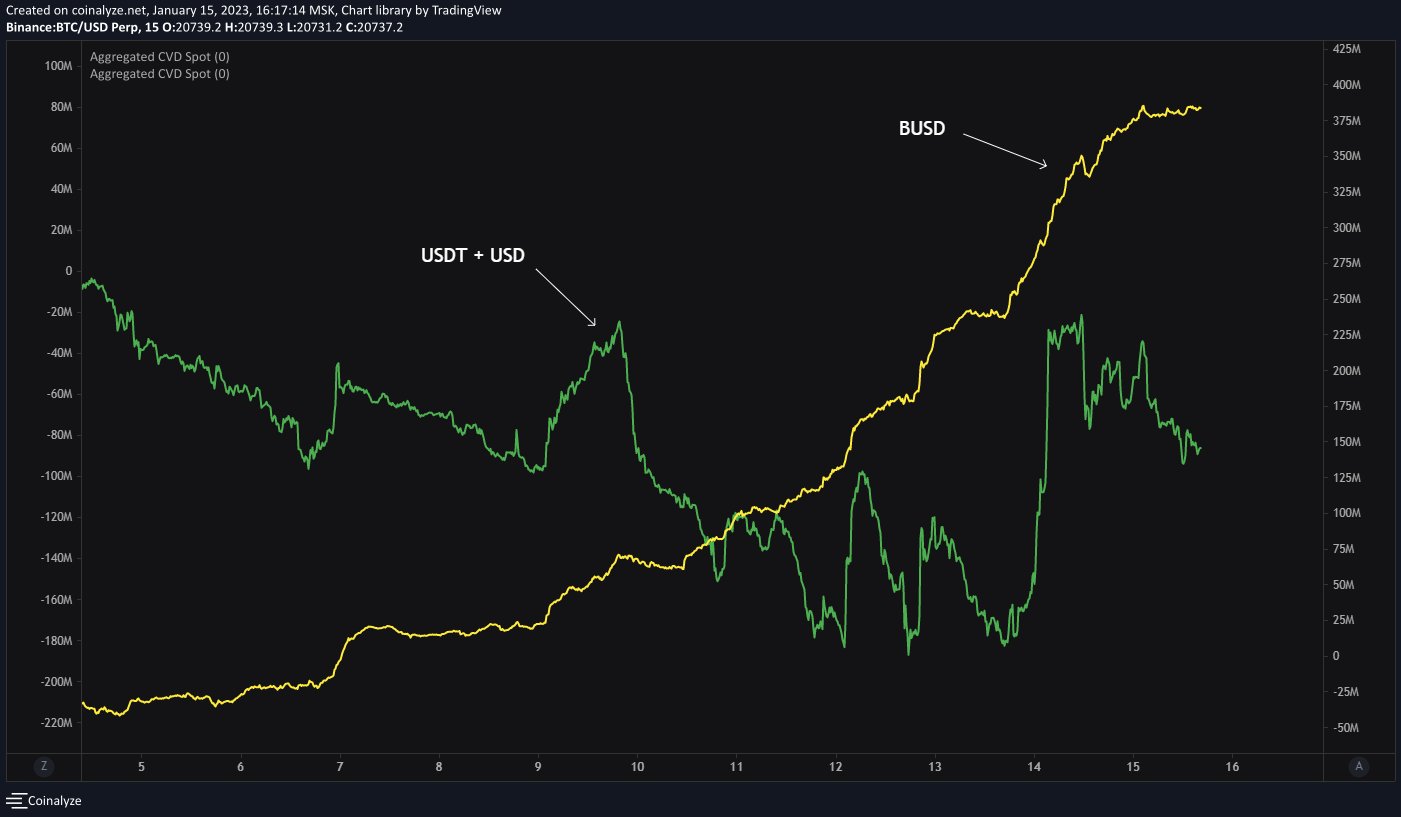

Bitcoin Price Manipulated By A Singe Entity At Binance?

Notably, rumors surfaced last week that the entire Bitcoin move from ,000 to ,000 was initiated by an entity at Binance. First, an anonymous trader pointed to the move being fueled by a BUSD stablecoin whale, citing the BTC Spot CVDs (Cumulative Volume Delta). On January 15, he shared the following chart and wrote:

Whole move from 17k to 21k was made by someone on Binance aggressively buying Bitcoin with BUSD. Other exchanges started to buy around 19.5k with USDT + USD. Green CVD includes all exchanges with Binance USDT as well, yellow CVD – only BUSD.

Yesterday, the trader wrote that both CVDs are showing a Bitcoin bearish divergences since yesterday. “Green line – spot CVD with all stablecoins including our loved one BUSD, blue line – perps CVD with all stablecoins as well. Looks like passive seller won this time,” the trader said.

However, the trader also clarified that while he was the first to report the huge BTC buying with BUSD on Binance, he never mentioned the words “cartel” or “manipulation.”

At press time, the Bitcoin price was once again attacking the ,000 level.