Over the past seven days, data reveals that the German government has transferred 3,820 BTC to cryptocurrency exchanges, with around 2,165.49 BTC moved in the last eight hours. German Government’s Bitcoin Transfers Cause Stir A week ago, Bitcoin.com News reported that the German government’s wallet, containing bitcoins seized from a piracy website, held 47,179 BTC […]

Over the past seven days, data reveals that the German government has transferred 3,820 BTC to cryptocurrency exchanges, with around 2,165.49 BTC moved in the last eight hours. German Government’s Bitcoin Transfers Cause Stir A week ago, Bitcoin.com News reported that the German government’s wallet, containing bitcoins seized from a piracy website, held 47,179 BTC […]

Bitcoin News

Bitcoin Selloff: German Gov’t Offloads Another $67 Million As Price Wobbles

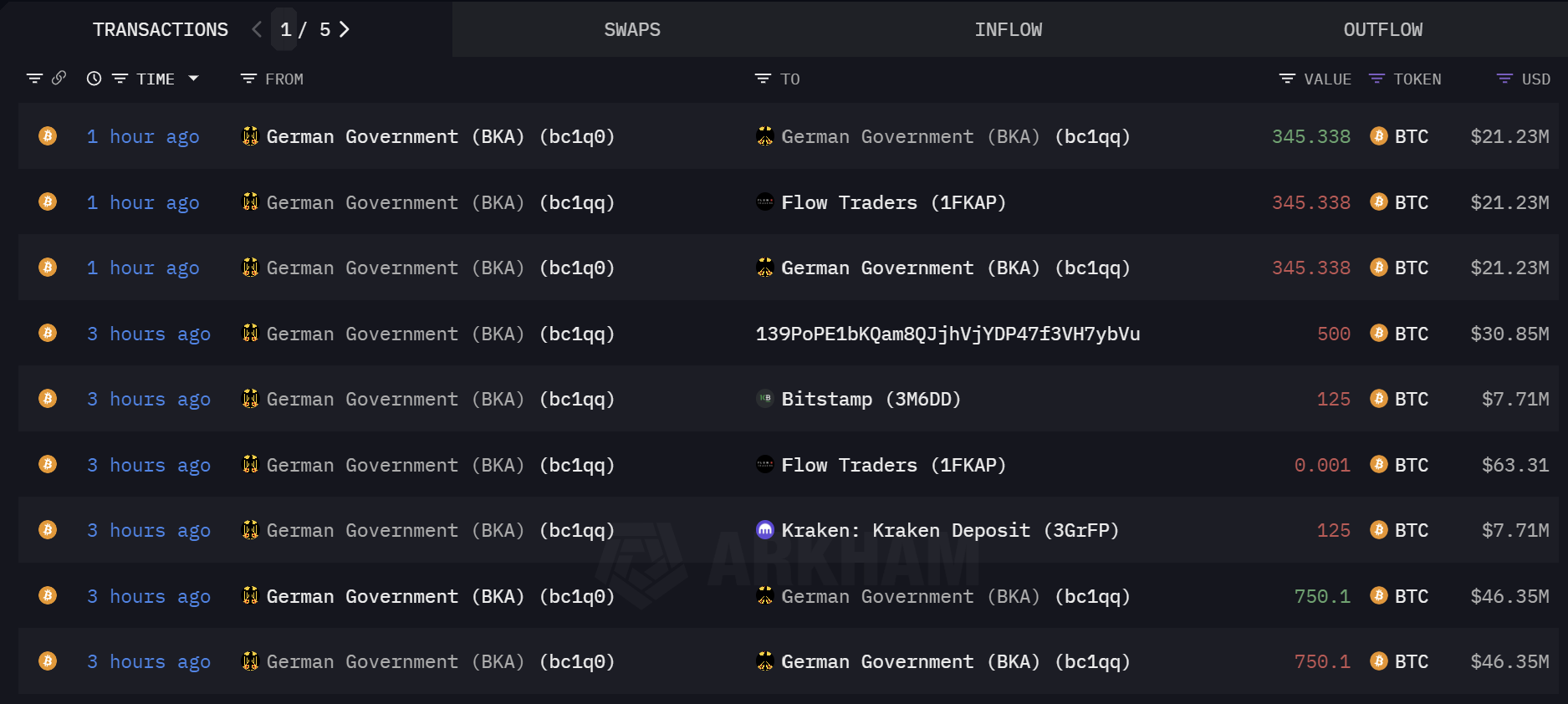

In a continued effort to liquidate its substantial Bitcoin holdings, the German government has once again engaged in significant transactions involving BTC, according to data from blockchain analytics platforms Arkham Intel. This morning, the Federal Criminal Police Office (BKA) executed nine transactions involving a total of roughly 2,786 BTC.

German Gov’t Continues Its Bitcoin Sell-Off

Arkham Intel’s data shows that four of them are internal transfers while five transactions were direct transfers to crypto exchanges and market makers, suggesting an intent to sell. The five potential sales amount to 1,095.339 BTC worth approximately million. Specifically, the BKA made two 125 BTC transfers, each worth approximately .7 million, to well-known crypt exchanges Bitstamp and Kraken.

An additional transaction involved a minute test transfer of 0.001 BTC to Flow Traders, a leading market maker. This small transaction was soon followed by a much larger transfer of 345.338 BTC to the same entity, strongly suggesting preparation for a substantial sell order.

Another noteworthy transfer of 500 BTC was directed to an enigmatic address tagged as “139Po.” This address has seen previous activity linked to the German government but remains shrouded in mystery, speculated to be another sale point.

These transactions form part of a broader trend observed since last week. Just a day prior, on June 25, the government had disposed of 400 Bitcoin worth million on Kraken and Coinbase, as well as 500 BTC to address “139Po.”

This is in addition to significant movements earlier last week: 0 million worth of BTC were transferred to exchanges on June 19 and million on June 20. Counterbalancing these outflows, the government received .1 million back from Kraken and .5 million from wallets associated with Robinhood, Bitstamp, and Coinbase.

Currently, the German government’s holdings amount to 45,264 BTC, valued at around .8 billion. This makes Germany one of the top nation-state holders of Bitcoin, trailing only behind the United States, China, and the United Kingdom, which hold 213,246 BTC, 190,000 BTC, and 61,000 BTC respectively, according to data from Bitcoin Treasuries.

BTC Price Hangs Above Critical Level

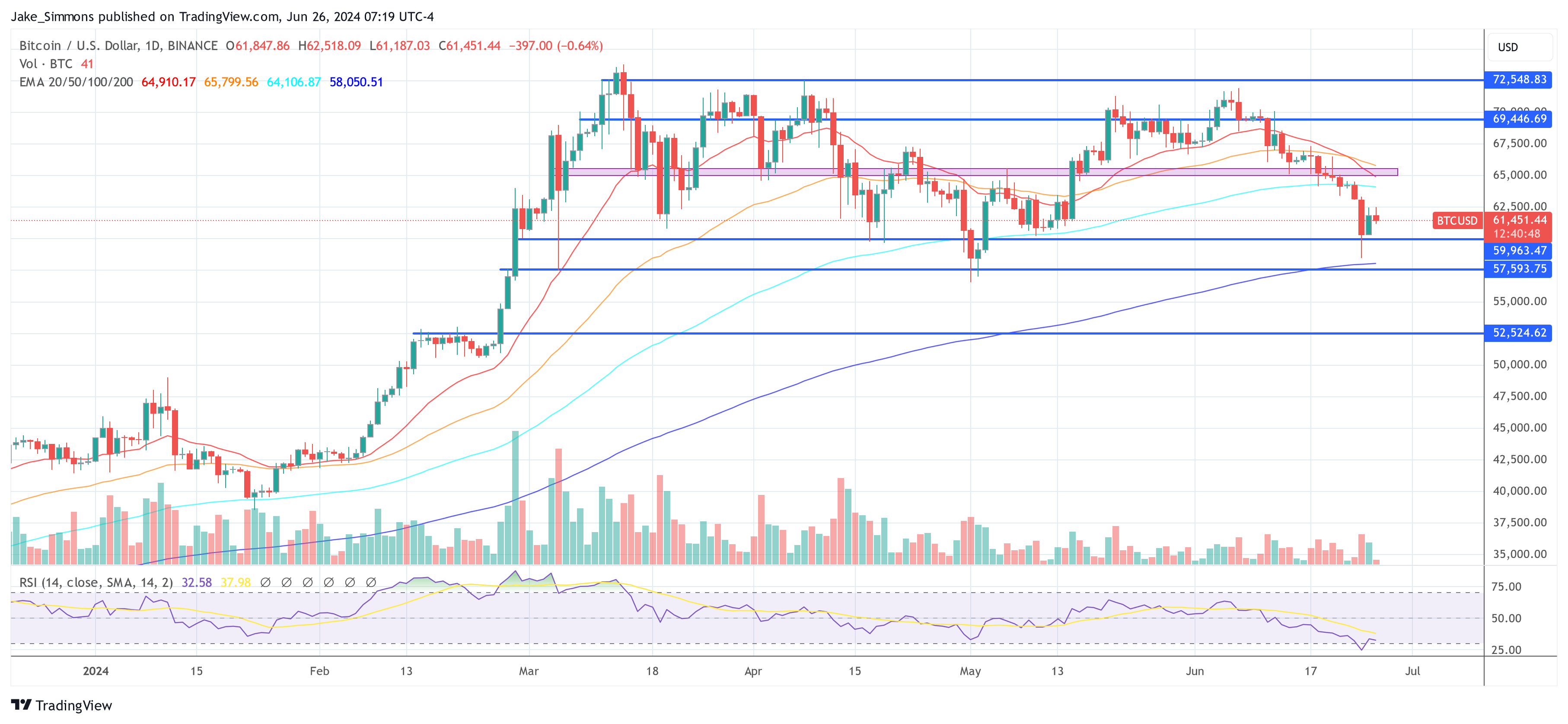

The pattern of large-scale disposals by the German government has contributed to fluctuations in Bitcoin’s market price, which has experienced a decline of approximately 6% since the onset of these transactions. Bitcoin’s value briefly fell below the ,000 threshold following the announcement from Mt. Gox about disbursing approximately billion worth of Bitcoin and Bitcoin Cash starting in July.

Market analysts and investors are also keenly observing these governmental actions as the sell-off seems to continue at a slow pace. This strategic liquidation by the German government arrives at a pivotal juncture for market sentiment, with Bitcoin prices teetering just above critical support levels. Should the daily trading price close below the ,000 threshold, it could potentially trigger a more pronounced downturn in Bitcoin’s price, exacerbating market volatility and uncertainty.

At press time, BTC traded at ,451.

Ethereum Whale Offloads Holdings Amidst Market Downturn

Ethereum (ETH) tumbled 6.45% in the past week, marking a rough stretch for the world’s second-largest cryptocurrency. Generally, Ether has left investors much to desire in recent times with a price decline of 16.57% over the last few months. Amidst this bearish market, a crypto whale has sold off all his Ethereum tokens drawing much attention from traders and market experts alike.

ETH Whale Liquidates Holdings, Incurs Substantial Loss

In an X post on May 11, blockchain tracking platform Lookonchain reported that a crypto whale offloaded all its 6,714 ETH tokens at a market price of .5 million. While the profit looks quite massive, LookonChain states that the investor actually recorded a loss of .5 million based on the acquisition price of these tokens.

Generally, whale transactions gain much attention among investors as they are viewed as indicators of market trends. Thus, if a whale suddenly sells a large portion or all of their holdings it may be interpreted as a bearish signal prompting other investors to follow suit, resulting in a price dip.

However, that may not necessarily be the case with the ETH market following this recent whale sell-off. With the Bitcoin halving completed in April, the crypto bull run is expected to begin in the following months based on historical data.

In previous times, Ethereum has proven as one of the most favorable assets for investors in this period. Notably, the altcoin gained by over 2000% in the months following the Bitcoin halving in 2020. Thus, most ETH investors are likely to hold on to their tokens.

Aside from Ethereum, the whale also liquidated all its 428,047 Optimism (OP) and 901,685 Arbitrum (ARB) at a loss of 2, 000 and .08 million respectively. In total, they incurred a loss of .43 million in offloading their investments in the three prominent altcoins.

ETH Price Overview

At the time of writing, ETH trades at ,919 reflecting a slight price gain of 0.27% in the last day. The altcoin appears to be heading for the $,2940 resistance zone. With sufficient buying pressure, ETH could push through this region with the next resistance level set at the 50 price zone.

However, the altcoin’s daily trading volume has currently declined by 44.85% falling to a value of .71 billion. Ethereum, which ranks as a bigger altcoin remains 40.4% off its all-time high value of ,891.70 achieved in November 2021z

FTX Estate Offloads $1.9 Billion Worth Of Locked Solana (SOL) Tokens In Sale

In a significant development, FTX bankruptcy trustees have reportedly sold about two-thirds of a .6 billion stash of Solana (SOL) at a “deeply discounted price.”

Industry figures such as Galaxy Trading and Pantera Capital were among the investors involved in the deal, according to people familiar with the matter, as reported by Bloomberg.

SOL Tokens’ Four-Year Journey

Per the report, the FTX estate was able to sell between 25 million and 30 million locked-up Solana coins at each, generating up to .9 billion in proceeds for the estate.

Under Mike Novogratz’s Galaxy Digital, Galaxy Trading managed to raise approximately 0 million for a fund established to purchase SOL from the FTX estate. According to the report, investors in the vehicle will be subject to a 1% management fee, and the investment will offer a yield through staking.

It is worth noting that the 41 million Solana tokens sold by the FTX estate are locked according to a pre-agreed vesting period, preventing them from being available for trading on the market.

According to Bloomberg, these tokens will gradually become available for sale over the course of four years, which could significantly impact SOL’s price action. However, as the tokens remain locked, SOL’s 739% year-to-date (YTD) uptrend remains intact, and the possibility for further gains remains in the cards.

Solana Sale Garners Interest From Prominent Figures

FTX co-founder Sam Bankman-Fried, convicted of fraud and sentenced to 25 years in prison, was a major supporter of SOL.

As previously reported, Bankman-Fried has actively engaged with guards at the Metropolitan Detention Center, where he is currently incarcerated. He offers investment advice and recommends SOL as a potential opportunity, demonstrating his bullish sentiment on the protocol.

The token, which operates on the Solana blockchain, constituted a significant portion of the digital assets stranded on the collapsed exchange, creating shockwaves throughout the crypto markets.

In addition to Galaxy Digital, Bloomberg notes that selling SOL tokens has attracted the attention of Pantera Capital. This .2 billion asset manager has reportedly raised capital for a special fund to acquire up to 0 million of SOL from the FTX estate.

Vancouver-based Neptune Digital Assets Corp. also announced the purchase of 26,964 SOL tokens for .7 million on March 27. However, FTX creditors are concerned they will be under-compensated in the SOL sale process.

Creditors Dispute FTX Bankruptcy Ruling

In January, the judge overseeing the bankruptcy case ruled that the amount of each claim should be based on what the customer or creditor was owed on the day FTX filed for bankruptcy. At that time, SOL was trading at about , well below its current market price.

As the price of SOL rallied in recent months, this discrepancy became a point of contention for some creditors. One creditor, Sunil Kavuri, expressed during Bankman-Fried’s final sentencing hearing that the SOL coins are “our property.”

Another creditor, whose name was redacted in court documents, stated in a written statement that the FTX estate is “giving away money for free to hedge funds.” In a recent interview, Bankman-Fried claimed the following regarding clients’ growing concerns about underpayment:

I’ve heard and seen the despair, frustration, and sense of betrayal from thousands of customers; they deserve to be paid in full, at current price. That could and should have happened in November 2022, and it could and should happen today. It’s excruciating to see them waiting, day after day.

Currently, the price of SOL stands at 5, reflecting a decrease of up to 6.7% within the last 24 hours and over 7% over the past week.

Featured image from Shutterstock, chart from TradingView.com

Ethereum Faces Market Tremors As Celsius Offloads $1 Billion in ETH

Ethereum (ETH) is about witnessing a potential sell-off worth billion. This significant transaction is rooted in actions by Celsius, a bankrupt crypto lender. Reports from on-chain analyst Lookonchain indicate that Celsius initiated the transfer of 459,561 ETH, estimated to be worth around .014 billion, to various exchanges.

The breakdown of this large-scale distribution includes 297,454 ETH (6.5 million) moved to Coinbase Prime, 146,507 ETH to Paxos Treasury, and smaller sums totaling 7,800 ETH (.2 million) sent to FalconX and Coinbase, respectively. Despite this transfer, Lookonchain disclosed that Celsius still maintains a reserve of 62,468 ETH, valued at roughly 9 million.

Celsius transferred 459,561 $ETH(.014B) out 9 hrs ago.

297,454 $ETH(6.5M) → #CoinbasePrime

146,507 $ETH (3.3M) → #PaxosTreasury

7,800 $ETH(.2M) → #FalconX

7,800 $ETH(.2M) → #Coinbase.And #Celsius still has 62,468 $ETH(9M) left.https://t.co/O71a2LfeKg pic.twitter.com/adcxQA3POn

— Lookonchain (@lookonchain) January 26, 2024

This significant transfer carries significant weight in the Ethereum market. It poses a challenge as it exerts considerable pressure on Ethereum’s price, with potential implications for broader market sentiment. Ethereum could see a significant plunge if the .014 billion worth of ETH is sold simultaneously.

Celsius’ Previous Ethereum Transactions

Celsius’ latest Ethereum transactions aren’t isolated events. LookonChain has previously spotted significant transfers linked to Celsius, including a deposit of 13,000 ETH ( million) on Coinbase and 2,200 ETH ( million) to FalconX.

While these moves indicate Celsius’ proactive strategy in managing its financial challenges, they also signal potential volatility for Ethereum’s market value.

Furthermore, Arkham Intelligence reports that between January 8 and January 12, Celsius liquidated over 5 million worth of Ethereum. The primary objective of these sales is to fulfill obligations to creditors.

Dune Analytics also highlighted the pattern of large-scale Ethereum redemptions, noting redemptions exceeding .6 billion. Since last year’s Shanghai update, this figure represents the highest Ethereum redemptions recorded.

As part of its bankruptcy proceedings, Celsius continues liquidating Ethereum holdings to pay off debts.

Ethereum’s Market Reaction

In the aftermath of Celsius’s Ethereum transactions, the asset has seen a nearly 10% decline in value over the past week, dropping from a high above ,600 to around ,186 yesterday. However, Ethereum has slightly recovered, rising by 2.2% in the past 24 hours, with a trading price of ,258 at the time of writing.

Amid these market developments, Michael van de Poppe, a renowned crypto analyst, has identified three key factors that could signal a bullish phase for ETH. A significant element is Bitcoin’s market behavior, often setting the tone for altcoins.

Van de Poppe notes that Bitcoin’s indications of bottoming out usually precede rallies in altcoins, suggesting a potential upturn for Ethereum. He also emphasizes the increasing excitement around spot Ethereum ETFs, which could catalyze Ethereum’s market value in the coming weeks.

Additionally, Ethereum’s impending network upgrades, which aim to reduce transaction costs significantly, are expected to enhance the network’s efficiency and scalability, potentially boosting its market appeal.

The momentum towards $ETH is probably going to come in the next few weeks.

Arguments:

– #Bitcoin bottoming out is a trigger for altcoins to make a new run.

– Ethereum Spot ETF hype.

– Ethereum launching new upgrades to reduce 90% of the costs. pic.twitter.com/N8bDi52F8M— Michaël van de Poppe (@CryptoMichNL) January 25, 2024

Featured image Unsplash, Chart from TradingView

Grayscale’s GBTC Offloads $527M in Bitcoin as Spot ETFs Record Lower Trading Volumes; Other Funds Continue BTC Accumulation

Based on the latest data, the recently introduced spot bitcoin exchange-traded funds (ETFs) experienced their lowest trading volume day since Jan. 11, 2024, recording roughly .28 billion in volume on Wednesday. Additionally, figures indicate that Grayscale’s Bitcoin Trust GBTC has offloaded another tranche of bitcoins, totaling 13,178.50 bitcoin valued at 7 million, in the last 24 hours.

Spot Bitcoin ETFs Hit Lowest Volume Since Jan. 11; Grayscale Unloads Over 13,000 Bitcoin, 9 New ETFs Hold .91B in Assets

As of Thursday, Jan. 25, Grayscale’s GBTC possesses 523,516.43 BTC, valued approximately at .71 billion based on the current BTC exchange rates. This figure is 13,178.50 BTC less than the previous day when the holding was 536,694.93 BTC. Consequently, since Jan. 12, 2024, GBTC’s bitcoin holdings have diminished by 93,563.56 bitcoin, equivalent to a value of .74 billion.

Despite Wednesday’s trading sessions being less vigorous than earlier days, GBTC remained a major player, commanding 0 million of the day’s total .28 billion in trading volume. In contrast, other spot bitcoin ETFs are steadily accumulating bitcoins. Blackrock’s IBIT currently possesses 45,668.08 BTC, valued at approximately .83 billion.

Fidelity’s FBTC has yet to update its daily figures, with the last recorded amount on Jan. 24 being 38,149.16 BTC. However, onchain metrics as of 8:00 a.m. Eastern Time on Thursday suggest FBTC now contains 39,319 BTC. On Wednesday, Ark Invest’s ETF had a holding of 12,880 BTC, which increased to 12,880 BTC by Thursday. Bitwise’s holdings remain static, with its address “1CKVs” continuing to secure 11,858.64 BTC.

Vaneck’s HODL ETF has experienced a modest rise, moving from 2,715.77 BTC to 2,772.33 BTC within a day. Similarly, Franklin Templeton’s EZBC has escalated from 1,305 BTC to 1,344 BTC. The Invesco Galaxy ETF, known as BTCO, maintains an estimated 6,339 BTC based on its assets under management (AUM). Valkyrie’s BRRR ETF has ascended from 2,201.50 BTC to a present total of 2,429.72 BTC, while Wisdomtree’s BTCW ETF has increased from 191 BTC to 201 BTC. Collectively, these newly launched spot bitcoin ETFs now hold a cumulative total of 122,831.77 BTC, worth an estimated .91 billion.

What do you think about the latest GBTC outflow and the accumulation from other ETFs? Share your thoughts and opinions about this subject in the comments section below.