According to data from June 3, an entity with eight wallets created in 2013 moved 200 BTC valued at .87 million after the funds remained untouched for over 11 years. If sold today, the value of these bitcoins has increased by 197,785% since their acquisition. Spending 200 Bitcoin Unveils Previous Transactions From 2013 On Monday, […]

According to data from June 3, an entity with eight wallets created in 2013 moved 200 BTC valued at .87 million after the funds remained untouched for over 11 years. If sold today, the value of these bitcoins has increased by 197,785% since their acquisition. Spending 200 Bitcoin Unveils Previous Transactions From 2013 On Monday, […]

Bitcoin News

GROK Memecoin Faces 40% Drop As Expert Exposes Scammer’s Involvement

Grok (GROK) token, inspired by Elon Musk’s artificial intelligence service through X (formerly Twitter), has recently come under scrutiny following explosive growth in market capitalization.

According to recent reports, Grok zoomed to a staggering 0 million market cap within just eight days of its release. However, reports of alleged scam involvement have overshadowed the token’s rapid ascent.

GROK Meteoric Rise Marred By Scammer Accusations

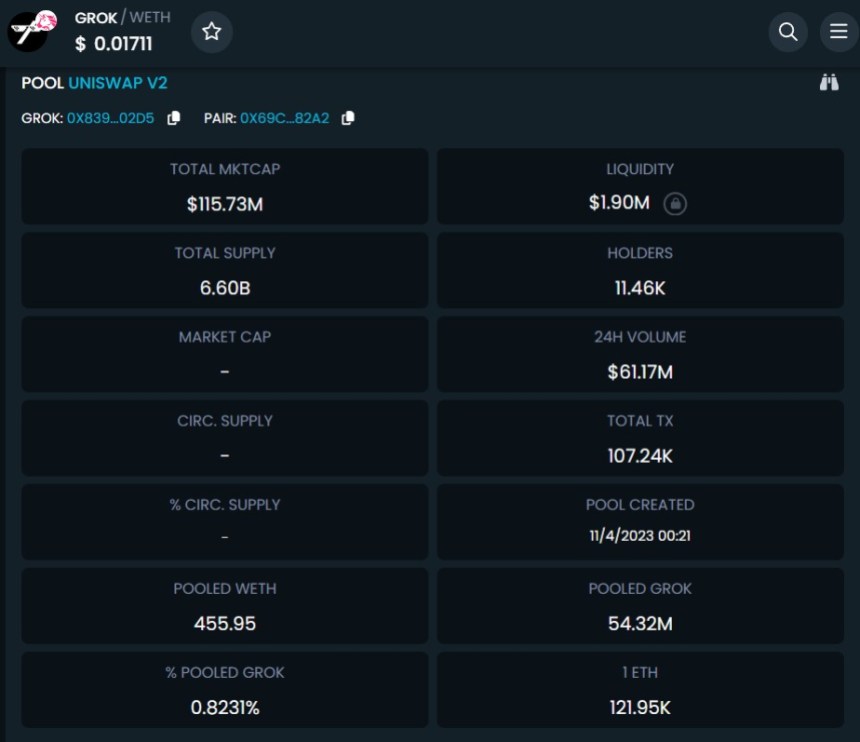

Grok token prices have soared, doubling within the past 24 hours alone, extending a week-long rally that has seen an astonishing 13,000% increase. The token boasts an impressive 11,000 holders and has witnessed a trading volume of over million over the past 24 hours, according to data from DEXTools.

However, ZachXBT, a self-proclaimed crypto detective, has raised concerns about the legitimacy of Grok, stating that the token was created by a scammer. ZachXBT has stated that the same X/Twitter account associated with Grok has been linked to at least one other fraudulent scheme. ZachXBT stated:

Not that people in this space will care but GROKERC20 GROK was created by a scammer. Same exact X/Twitter account has been reused for at least one other scam. X/Twitter ID: 1690060301465714692

Satoshi Flipper, another prominent crypto trader on X, echoed this sentiment, labeling Grok as an “effing scam” and emphasizing that Elon Musk did not authorize the token’s launch. Satoshi Flipper said:

This is Grok. .9M liquidity and a 7M market cap? What an effing scam. Not only that, it’s completely fraudulent to trade this knowing Elon Musk, the owner of Grok, did not authorize these devs to launch a token. Imagine touching this toxic trash.

Experts from Arkham Intelligence also weighed in, reporting that an on-chain trader sold a significant amount of GROK at nearly 40% slippage, reinforcing the scam allegations made by ZachXBT.

The controversy surrounding Grok has raised concerns within the cryptocurrency community. Critics argue that the token’s market cap, coupled with the lack of authorization from Elon Musk, raises red flags.

Impressive Turnaround

The token’s market cap has undergone a retracement, now at 8 million, down from its previous value of 0 million. Additionally, the token exhibits a liquidity of .83 million.

Despite experiencing a substantial slippage of 48%, with its price dropping as low as .0056000, the token has remarkably recuperated and is now trading at .0108452.

It is yet to be determined whether further reports will surface to shed light on the individuals behind the token’s creation and their objectives, potentially exposing the risk of a rug pull within the cryptocurrency industry.

However, despite these allegations, the token has attracted significant attention and excitement from investors eager to participate in the potential surge of the next major meme coin, aiming to achieve substantial gains in their investments. As of the time of writing, the Grok official account on X has not made any statements regarding these allegations.

Featured image from Shutterstock, chart from TradingView.com

Report Exposes Warrantless Cash Searches at Atlanta Airport

In a startling investigation report, Atlanta News First uncovered the concerning practices of the U.S. Drug Enforcement Administration (DEA) task force officers. At Hartsfield-Jackson Atlanta International Airport, DEA officers, in plain clothes, have been found searching passengers’ carry-ons without warrants and seizing large sums of cash without making arrests. The report and attorneys say the practice raises constitutional and privacy concerns among American citizens.

Plainclothes Cash Hunts at Airports

Atlanta News First recently shadowed DEA task force officers at Hartsfield-Jackson, observing them as they discreetly moved from gate to gate. Passengers were searched right after scanning their boarding passes, often without any clear indication of the officers’ actual identity or purpose.

Film director Tabari Sturdivant recounted his unsettling experience. Mistaking a DEA agent for a Delta representative due to displayed airport credentials, he said, “He just approached me, and he asked me for my ID. He didn’t state who he was. He just asked me for ID, and I thought he was a Delta agent. He had airport credentials on, and so I gave it to him immediately.”

The filmmaker noted that the DEA agents didn’t find anything suspicious but asked him:

Are you high? Have you smoked? Do you have any drugs in this bag? Do you have any money?

Warrantless searches and seizures directly violate the Fourth Amendment, which is aimed at safeguarding American citizens from such unreasonable intrusions. The report notes that these actions by DEA agents not only infringe on personal freedoms but also erode the public’s trust in law enforcement agencies.

This isn’t the first episode of the DEA and law enforcement authorities unlawfully seizing individuals’ assets. Take, for example, the DEA’s extensive track record of orchestrating “cold consent encounters” at Amtrak stations, mirroring their tactics at airports. In 2021, FBI agents confiscated million from safety deposit boxes in Beverly Hills, a move attorneys decried as lacking proper justification.

A report by Reason reveals that, over the past decade, law enforcement, with the DEA at the forefront, has seized a staggering billion in cash. Data from the Department of Justice’s Office of the Inspector General (OIG) indicates that about 65,000 cash seizures, representing 81%, were subjected to administrative forfeiture by the DEA, amounting to .2 billion.

Atlanta News First highlights that film director Sturdivant represents just a fraction of those scrutinized for cash by undercover officers at the airport. The investigative piece also points a finger at Clayton County narcotics officers. The news team found “several similar cases where officers with the DEA task force or Clayton County Police searched innocent people or seized money without making any arrests.”

In 2023, carrying significant cash amounts is increasingly viewed with suspicion, even if earned rightfully with proven receipts. Constitutionalists and lawyers insist that law enforcement’s propensity to outright confiscate these life savings, without just cause, is a disturbing trend.

What do you think about the report about the Atlanta airport searches? Share your thoughts and opinions about this subject in the comments section below.

New Documentary Exposes the Turbulent Downfall of FTX and Sam Bankman-Fried

According to Bloomberg, the media firm plans to release an eye-opening documentary on Sam Bankman-Fried and the shocking downfall of his once-prominent exchange FTX. The film, “Ruin: Money, Ego and Deception at FTX,” is slated for an October 26 debut. It promises a deep dive into the staggering breakdown of FTX, Alameda Research, and the leadership – or lack thereof – behind these fallen crypto companies.

A Wave of Cinematic Takes on Sam Bankman-Fried Set to Flood Screens Soon

Bloomberg is gearing up to unveil one of the first documentaries delving into Sam Bankman-Fried (SBF) and FTX’s saga. This Bloomberg Originals production casts a spotlight on the “dramatic downfall of his cryptocurrency enterprise.”

The narrative brings together journalists from Bloomberg and industry insiders, unraveling the exchange’s decline and the current legal storm surrounding SBF. The media outlet plans to publish the SBF documentary on October 25, 2023, at 6 p.m. (ET).

A trailer, just over two minutes, has also made its debut on October 13. This unveiling coincides with SBF navigating the treacherous waters of his New York trial, where he confronts testimonies from former allies like Caroline Ellison and Gary Wang.

These former associates have painted a damning picture, alleging SBF directed them into fraudulent activities and greenlit Alameda’s mingling with FTX’s client funds. Amidst this media frenzy, acclaimed “Big Short” author Michael Lewis is on a promotional spree for his latest offering, “Going Infinite: The Rise and Fall of a New Tycoon.”

Buzz suggests that Apple has snatched the cinematic and TV rights, with studio XTR purportedly crafting an FTX and SBF film as well. Furthermore, sources hint that The Information and Vice Media are pooling resources to sculpt an SBF cinematic portrait.

However, as the courtroom drama unfolds, questions swirl around the veracity of these on-screen renditions. With SBF’s trial still in play, he could either walk free or face years in prison.

Lewis’s tome, despite its completion, hasn’t been spared from criticism. Especially contentious was his claim on “60 Minutes” that FTX “actually had a great real business.”

Such assertions starkly clash with the recent testimonies of Ellison and Wang. Nonetheless, with all these biopics coming, audiences are in for a whirlwind tale encompassing vast fortunes, hedonistic indulgences, polyamorous relationships, and layers of deceit.

What do you think about Bloomberg’s upcoming SBF and FTX documentary film? Share your thoughts and opinions about this subject in the comments section below.

Ex-Alameda Employee Exposes Firm’s Massive Bitcoin Trading Misstep

An ex-employee of Alameda Research has revealed that a trading blunder from the firm precipitated an astonishing 87% plunge in bitcoin’s (BTC) price on the Binance US exchange. This mishap, the insider disclosed, resulted in losses reaching the “order of tens of millions.”

An Alameda Trader’s ‘Fat Fingers’ Triggered a Flash Crash on Binance US in 2021

A past associate of Sam Bankman-Fried’s crypto trading entity, Alameda Research, has been candid about his experiences within the firm. Aditya Baradwaj, on August 23, recounted that during his engineering tenure at Alameda, he saw his “entire life savings stolen”, pointing fingers at Bankman-Fried. Baradwaj shared that in his 18 months at Alameda, his personal and professional trajectory shifted dramatically.

Fast forward to September 20, Baradwaj delved into an incident from October 21, 2021. On that day, bitcoin’s (BTC) valuation flash crashed by a staggering 87% on Binance US, only to rebound shortly after. He recounted that an Alameda employee mistakenly placed an erroneous order, describing it as a “slip of a finger.”

“The trader was trying to sell a block of BTC in response to news, and sent out the order via our manual trading system,” Baradwaj stated. “What they missed was the decimal point was off by a few spaces. Rather than selling BTC at the current market price, they sold it for pennies on the dollar.”

Baradwaj added:

News outlets started picking up too. Binance US – which was the epicenter of the flash crash – released a statement claiming that it had been caused by one of their ‘institutional traders’ who had a ‘bug in their trading algorithm.’ I guess Caroline had made some phone calls.

This isn’t Alameda’s maiden public faux pas or CEO Caroline Ellison‘s. As recently as December 2022, a whistle-blower from FTX informed Bitcoin.com News about Ellison’s margin account sinking by .3 billion in May 2022.

During a conversation with Jen Wieczner from New York Magazine, Sam Bankman-Fried opened up about a particular margin position that became untenably large. He emphasized that the sheer size of Alameda’s margin meant it “was not going to be closable in a liquid way in order to make good on its obligations.”

What do you think about the ex-Alameda employee’s memory of the bad bitcoin trade? Share your thoughts and opinions about this subject in the comments section below.

Ex-Alameda CEO Caroline Ellison’s Google Docs Diary Exposes Struggles Prior to FTX Collapse

According to the New York Times and several sources familiar with the matter, Caroline Ellison, former CEO of Alameda Research, maintained a diary on Google Documents that provides a brief glimpse into the challenges she faced before the collapse of FTX. Excerpts from the diary suggest Ellison lacked confidence in her role. After her breakup with Sam Bankman-Fried, FTX co-founder, her enthusiasm for Alameda “significantly decreased.”

Ellison Didn’t Think She Was Well Suited to Lead Alameda Research

Caroline Ellison, former CEO of Alameda Research, a quantitative trading firm owned by Sam Bankman-Fried, reportedly maintained a diary on Google Documents. The New York Times, in a report dated July 20, 2023, confirmed with four people familiar with the matter that the publication reviewed the documents.

Attorneys involved in the case against Bankman-Fried have allegedly circulated these Google documents in court. Ellison’s diary provides insight into her personal and professional life while working under the now-defunct FTX cryptocurrency empire.

In February 2022, Ellison expressed her dissatisfaction and overwhelmed feelings in regard to her job. “At the end of the day I can’t wait to go home and turn off my phone and have a drink and get away from it all,” she said.

Diary excerpts note a romantic relationship between she and Bankman-Fried, adding an element of “weirdness” and causing “drama.” In one document, Ellison further explained her belief that she was not qualified to serve as Alameda’s chief executive. Ellison wrote:

Running Alameda doesn’t feel like something I’m that comparatively advantaged at or well suited to do.

According to the report, when Bankman-Fried’s billion empire collapsed, Ellison expressed relief that the chaos was ending. “I just had an increasing dread of this day that was weighing on me,” Ellison wrote. “Now that it’s actually happening it just feels great to get it over with.”

Ellison is scheduled to testify against Bankman-Fried in his October trial, along with two other coworkers. In her testimony, published in December 2022, she alleged that Bankman-Fried had instructed her to commingle customer funds since 2019. Furthermore, it’s possible that Ellison underperformed in her role at the quantitative trading firm and may have held an FTX margin position that was negative .3 billion in May 2022.

What do you think about Caroline Ellison’s alleged Google Documents diary excerpts? Share your thoughts and opinions about this subject in the comments section below.

Buying a Tesla With Bitcoin Exposes This Flaw, Don’t Get Caught Out

In February, electric car maker Tesla announced it had purchased .5bn in Bitcoin. Along with the announcement was a commitment, they would also accept BTC as payment, making it the first car manufacturer to do so.

The firm followed through with that pledge. As of yesterday, using Bitcoin to buy directly from Tesla became a reality. But a look at the terms and conditions highlights a situation that makes little sense for buyers.

Why is Buying a Tesla With Bitcoin a Bad Idea?

Given Elon Musk’s interest in cryptocurrency, it was only a matter of time before Tesla would accept Bitcoin. While some say this is good for crypto, a deeper dive shows it may not be good for consumers.

The main problem is that Tesla uses dollar pricing and then converts it into a Bitcoin price payable. Considering the volatile nature of cryptocurrencies, customers could pay significantly different BTC amounts for the same thing.

“All products are priced in U.S. Dollars. If you choose to make a payment using Bitcoin, you must pay an amount of Bitcoin that is of equivalent value to the U.S. Dollar purchase price of the product that you purchase.”

A further issue arises in the case of refunds and buybacks. According to the terms and conditions, Tesla can choose to refund you in either the exact Bitcoin price at the time of purchase or the dollar equivalent.

“If you are entitled to a refund of your payment or to a buyback, we reserve the right to refund to you either the exact Bitcoin Price that you provided to us at the time of purchase or an amount of US Dollars that is equivalent to the US Dollar price of the product that you purchased, at our sole and absolute discretion, taking into consideration operational efficiency.”

Refunding customers in Bitcoin exposes buyers to market dips. While it’s likely Tesla would refund in dollars if the market rose between purchase and refund dates.

Add to this capital gains tax obligations when buying in Bitcoin, and paying in dollars looks the better deal.

Musk Doesn’t Want Dollars

Elon Musk revealed the firm plans to keep the Bitcoin earned rather than convert it to dollars.

“Tesla is using only internal & open source software & operates Bitcoin nodes directly.

Bitcoin paid to Tesla will be retained as Bitcoin, not converted to fiat currency.”

As ever, his response triggers more questions than it answers. For example, does Musk believe the dollar will devalue substantially? And why is Tesla running Bitcoin nodes? Especially when there is no financial reward for doing so.

In any case, buying a Tesla with Bitcoin only works if the car is priced in Bitcoin. Considering most supply and expense ecosystems operate in dollars, pricing in Bitcoin won’t happen anytime soon.

Source: BTCUSD on TradingView.com

Bitcoin Dominance Exposes Altcoins To Bounce or Die Scenario

Over the last month, Bitcoin dominance has grown by nearly 3%. The climb has largely been driven by the asset’s block reward halving set for less than 24 hours from now.

The latest move in BTC dominance has left altcoins on the ropes, and exposing them to a bounce or die scenario. The apex of a multi-year triangle is nearing a resolution, and which way it breaks will determine the future of the alternative crypto assets. Is this the asset’s make it or break it moment?

Bitcoin Dominance Forms Multi-Year Triangle, Price Action Reaches Apex

BTC dominance is a metric used to weigh the first-ever cryptocurrency against the rest of the market.

Increases in the market caps of altcoins such as Ethereum, Ripple, or Chainlink lower Bitcoin’s dominance over the rest of the space.

Related Reading | This Altcoin’s Fractal Shows How Epic the Next Crypto Bull Market Can Be

Just like price charts of individual assets, BTC dominance ebbs and flows just like anything else. During altcoin seasons, BTC dominance takes a dive. However, when things get especially bullish for Bitcoin, altcoins often suffer as a result.

Take last year’s bull run for example. Altcoins had performed strongly aside Bitcoin, until around May 2019 and then Bitcoin left them in its dust.

Alts crashed, and Bitcoin set a local high. BTC dominance reached a high of 73% before reversing.

Bitcoin is once again performing, and its halving is tomorrow. The bullish event could lead Bitcoin to break free from a separate long-term triangle on the BTCUSD pair. This would also cause a corresponding break of the triangle on BTC.D charts.

And with the most recent price action leaning heavily bullish towards Bitcoin, altcoins could see a major collapse.

BTC Dominance: Will Altcoins Skyrocket Again, or Will They Be Annihilated

In the above chart, the total altcoin market cap can be seen as a trading pair against BTC. The chart essentially acts as the inverse of a BTC.D chart.

A breakdown of the multi-year triangle could result in complete destruction to altcoins that are already down over 99% in many cases.

Related Reading | Bitcoin Dominance Climbs, Leaving Altcoins Vulnerable to New Leg Down

However, symmetrical triangles also can break up. With the prior trend being bullish for altcoins, continuation to the upside is very likely.

Clearly, given the circumstances, altcoins are at a bounce or die junction that will shape the future of the asset class.

Bitcoin’s halving is tomorrow, and the asset is expected to explode into its next bull market as a result. But it was the last halving that kickstarted the alt season that sent the assets to their all-time highs.

In the below BTC.D chart, each halving has been highlighted with a red dotted line.

The 2016 halving is what sent altcoins into the stratosphere, causing BTC.D to dip from a then-high of 98% to as low as 35% as the crypto bubble of 2017 peaked.

Is the cycle restarting once again with the halving, or will Bitcoin‘s bull run crush altcoins once again?

NewsBTC

Crypto Market Crash Exposes Shortcomings of Various Exchanges

The global economy is currently under tremendous pressure, thanks to the fast-spreading COVID-19 pandemic, the OPEC fueled oil price war, global stock markets shock and more. The widespread issues have driven global stock markets, futures and crude oil prices to the ground and spread into the cryptocurrency market as well.

Considered the best alternative and one of the safe havens during tumultuous economic times, the cryptocurrency market wasn’t immune to the onslaught either. After coming under heavy selling pressure, the price of BTC, which was at a new high of recent times at ,502 over a month ago on Feb 13, 2020, plunged on Mar 13, wiping off 44% of its value in just a few hours. On that fateful day, the benchmark crypto fell to a low of ,791.9.

While the price rebounded to around ,000-mark, Bitcoin is still struggling to recover the lost ground. It is not just the Bitcoin that bore the burnt, the world’s top 10 cryptocurrencies witnessed a fall in their market cap by over 30% with USDT- only stablecoin among the top 10 being an exception.

The sudden fall in cryptocurrency prices sent out shockwaves through the entire industry, as exchanges and trading platforms had to deal with a sudden influx of users trying to sell off and hedge. As orders started flooding in, the market depth and capacity of the trading systems were put to the test. The performance of these exchanges under such situations also offered an insight into their efficiency and reliability.

Some Exchanges Performed Better than the Rest

Many exchanges over the weekend witnessed their performance impacted due to sudden market movements. These problems ranged from delayed spot depth push to overloaded futures trading system. On one leading exchange, the problem was accompanied by the failure of the futures ADL system. There were also claims that the exchange raised ETH withdrawal fees to stem the outflow of funds.

Server errors, downtime in futures and OTC trading were also prevalent across almost all exchange during that time. The flaws in the market depth on a few exchanges was exposed to be way less than the claims, and some robust exchanges like OKEx experienced app lag. Even though all these issues were a result of an unexpected turn of events, the trading community was inconvenienced. It is to be seen whether the traders will make any changes in the trading patterns or platform preferences after having experienced the market shock.

Few Good Things During Bad Times

The price crash is just a temporary setback, as most people in the crypto already know or have experienced in the past. The cryptocurrencies, especially BTC, are expected to regain the lost ground and even soar above this year’s maximum price in the coming months. In the past couple of days, the BTC futures trading volumes have gained ground with billion worth of trading on OKEx alone. According to Skew data, OKEx has gained the top spot in terms of BTC Futures volume followed by BitMEX, Huobi Binance, bybit and others.

According to the Jay Hao CEO of OKEx, the platform and its trading services were able to process as many as 300k orders per second during the volatile period while maintaining a record of 0 clawbacks during the market crash.

Also, just because the cryptocurrency price is falling doesn’t mean every investor is making losses. Those who opt for derivatives can still profit during the downturn by formulating different trading strategies. Multiplex derivatives trading tools can help with hedging and shorting to reduce losses and even make profits in the process. OKEx users have access to a full suite of crypto trading products, including spot with margin trading, options trading, futures and perpetual swaps, allowing them to pick the right one to match prevailing market conditions. The best example in today’s highly volatile situation is the opportunity BTCUSD options trading offers for the users to reap profits.

Irrespective of the general sentiment in today’s markets, there is still a lot of hope left for cryptocurrencies. With governments actively introducing fiscal policies to contain the economic situation, the crypto market is benefit from it. Meanwhile, various industries and governments are looking for ways to incorporate blockchain technology into the existing systems, with some economists even calling for the creation of fiat-backed central bank-issued cryptocurrencies to promote financial inclusion and wellness. Even Lennix Lai from OKEx has, on multiple occasions, expressed the idea of using some stablecoin and blockchain to eliminate unbankedness, which received a positive response from various government representatives.

The crypto market crash is neither the first nor the last time in the over-a-decade-old legacy of Bitcoin and other cryptocurrencies. But each time, the market has bounced back stronger than ever before. Until then, all one can do is wait and trade responsibly with the right strategies.

NewsBTC

China’s State Outlet Xinhua Exposes Millions to Bitcoin

China doesn’t seem to want the Bitcoin and blockchain gravy down to slow down any time soon. On Sunday afternoon (PST), reports arose on Twitter that Chinese state media had begun to talk up the leading cryptocurrency via an article. While the price of BTC hasn’t reacted to this tidbit of news, this article could have a resounding effect on China’s knowledge of crypto assets in the coming years.

Related Reading: Chinese Bank Invests in Bitcoin Wallet After President Xi’s Remarks: Report

Chinese State Media Talks Up Bitcoin

Monday’s edition of Xinhua — the official state-run publication of the People’s Republic of China — contained an article whose title roughly translates “Bitcoin: The First Successful Application of Blockchain Technology.” While the piece wasn’t all positive, the headline alone may push Chinese investors to take a close look at the cryptocurrency market once again, despite the restrictions put in place.

Chinese state newspaper today (Xinhua)

Bitcoin: The First Successful Application of Blockchain Technologyhttps://t.co/85icR9FcAH pic.twitter.com/8ZOF6UBSzw

— Matthew Graham (@mg0314a) November 11, 2019

The full-page article was shared by Matthew Graham of Sino Global Capital. According to Graham’s digital translator, the piece calls Bitcoin a non-tangible currency and a “currency” in quotation marks — whatever that implies. The Xinhua article also mentioned how blockchain technologies work, including the mining process halvings.

There aren’t any concrete statistics about the readership of Xinhua, but it likely ranges in the dozens of millions.

Not the First Time…

This isn’t the first time Chinese media and large corporations/banks have lauded Bitcoin.

Earlier this year, The Bank of China — decisively not to be confused with China’s central bank, the similarly-named People’s Bank of China — was reported to have published an elaborate article about the many facets of Bitcoin.

Yesterday the #BankofChina posted up an article about #Bitcoin. They explained how $BTC works, why the price is going up, and why it’s valuable. Never thought I’d see that happen.

#Bullish pic.twitter.com/GKzj7XJjJa

— Samson Mow (@Excellion) July 27, 2019

According to a read and rough translation of the article by Blockstream’s CSO, Samson Mow, the institution — the four biggest state-owned commercial banks in China — mentioned how Bitcoin works, why the price of cryptocurrencies are rising, and why BTC inherently has value.

That was far from the end of it. An infographic contained in the post portrayed key points in the history of the Bitcoin industry; it specifically made mention of the “Bitcoin Pizza Guy” story, Warren Buffett’s scathing remarks about digital assets, the supply limit of BTC, and the price action seen over recent years.

Related Reading: No, China Isn’t Banning Bitcoin Mining: Chinese Crypto Insider

Considering that just a year ago, it was verboten — with reports circulating that cryptocurrencies were somewhat taboo on certain forums — it’s crazy to see how far the Chinese cryptocurrency space has come.

Featured Image from Shutterstock

The post China’s State Outlet Xinhua Exposes Millions to Bitcoin appeared first on NewsBTC.